Pulling Back the Veil Part II: Surveying Insurance Struggles

In too deep

Last January, my phone rang. My credit card company alerted me that my credit card was being placed on hold due to a $13k potentially fraudulent charge. The call was followed within seconds by the pharmacy who wanted me to know they were unable to process my prescriptions without authorization. Our quarterly bill for insulin and test strips was $13k—full retail price. It turns out that none of our prescriptions were covered without pre-authorizations and appeals. We were fortunate that our credit card company stopped the transaction. With increasing deductibles, I did not have $13k available that most likely would not be reimbursed after pre-authorizations. I spent two months living on our hoarded supplies and figuring-out different paths to get the medications we needed—many are highlighted at No Small Voice—including 340b Programs. I was able to successfully appeal 12 of my 13 denied insurance claims.

Survey says…

This information below is based on survey results for people living with type 1 diabetes (T1D) and includes helpful advice. I also believe it is relevant for people living with type 2 diabetes (T2D). While things seem complicated and you are not certain you can make it through one more phone call with your insurance company, I am asking you to dig deep and keep pushing forward. The reality is if you keep pushing, you have a good chance of being successful.

- If you receive a denied insurance claim, you should definitely appeal. Our survey showed a 78 percent chance of getting the claim approved. The one big exception we would highlight—we have not found any adult who has successfully completed an appeal with UnitedHealthcare for a non-Medtronic pump.

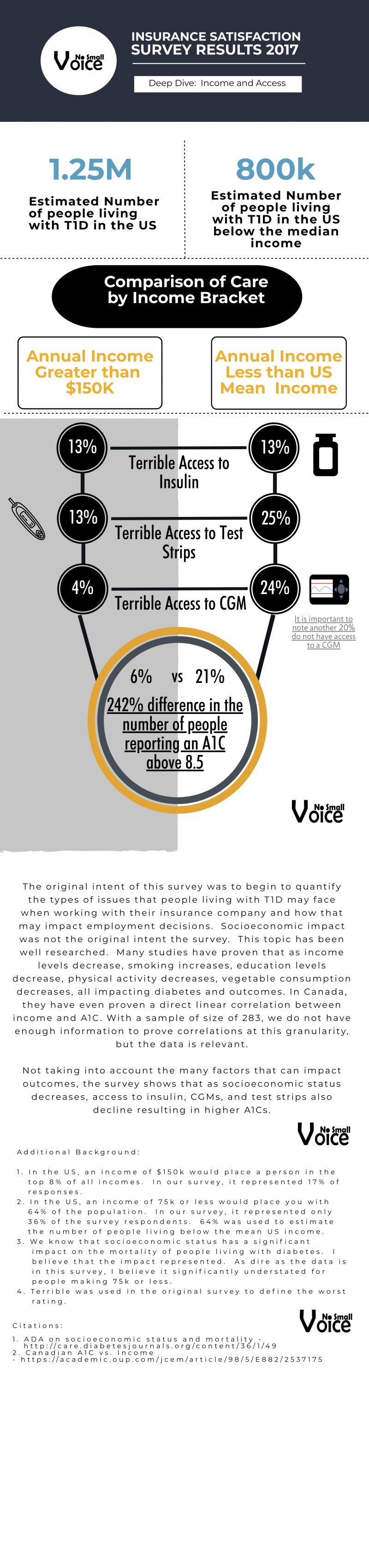

- Lots of research has shown factors that impact outcomes. Smoking, exercise, age and income level impact A1Cs. In our data, a person making $75k or less was 264 percent more likely to have an A1C above 8.5%. This group reported the highest level of difficulty accessing test strips and continuous glucose monitors (CGMs). It was surprising that ALL income ranges reported the same level of difficulty accessing insulin.

- As the number of denied insurance claims increased, A1Cs also increased for people who appealed the denied claims. This finding was not published earlier due to small sample size. It is important to highlight this preliminary finding because it is new, and adds to the list of issues that impact patient outcomes. Obstacles impact access leaving patients scrambling to get the prescriptions they need, taking away time needed to manage their chronic illness, including rest, and increasing the burden of patient care. It only seems logical for every obstacle a person living with T1D encounters that there is a direct impact to their well-being.

- If you have insurance, it is likely you will be faced with a challenge—multiple phone calls to resolve issues, pre-authorization, prescriptions not available on a plan and cost. Make sure you have a plan to address these challenges.

- Despite everyone’s best attempt at getting information during open enrollment, 66 percent strongly disagreed that they had the information required to make a decision for their insurance. This lack of information is most likely the cause for many of the challenges faced. During open enrollment, ask for a copy of your formulary and overview of projected costs. In the right circumstance, you may want to share your open enrollment experience with your HR department.

People are concerned about what their employers will think. They feel embarrassed to be highlighting their inability to afford life-saving medications. A few brave people like Dillon Hooley and his family are openly sharing their stories. Many people face similar challenges but find strength and value in telling the story as a community. I am asking for your support to continue to tell our community’s story.

This ongoing survey is currently available—you can access it here.

Read Part I of Pulling Back the Veil here.

{kind=link}